In the 1970s, my father frequently captured moments on his Canon Super8 camera. He filmed his first car, his friends, skiing stunts, and his daily life as a crew member aboard the MS Nordtrans Vision. As a history enthusiast, my personal favorite is the footage of him crossing the Suez Canal in 1975, right after its long-awaited reopening. I cherish it not only for its uniqueness but also as a high-quality record of a pivotal historical event.

Recently, as I watched this film, it prompted me to reflect on current geopolitical events. The global tension, stemming from ongoing wars in Europe and the Middle East, is palpable. It’s evident not only in news headlines but also in the atmosphere of major cities worldwide. It’s reminiscent of the tense times in the 1970s.

In this post, I want to share my thoughts on a scenario that’s been on my mind, given the intricate dynamics of the ongoing conflict in the Middle East. What would be the consequences of a regional war, or even a hypothetical closure of the Suez Canal in today’s world?

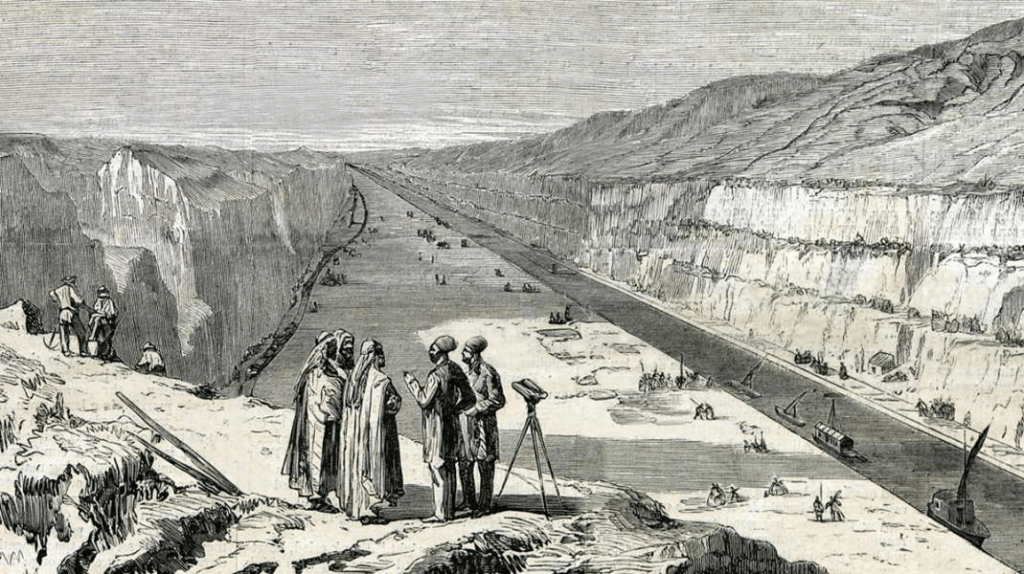

The Suez Canal, opened in 1869, serves as a pivotal maritime passageway connecting the Mediterranean Sea to the Red Sea. Throughout its history, it has been at the epicenter of several significant closures and disruptions. These events have had profound ramifications on global trade and the economy, with consequences reverberating across multiple industries.

One can’t help but draw parallels from current geopolitical tensions to past events that shook the world. Notable examples from history are the closures of the Suez Canal in the mid-20th century. The canal’s shutdowns, both brief and prolonged, had ripple effects across the global shipping industry.

In this article, I’ll delve into two specific closures: those in 1956 and from 1967 to 1975. Despite being centered around the same canal, these events had distinctly different impacts on international trade and the world economy due to their differing durations, causes, and geopolitical backdrops.

In 1956, the Suez Canal was temporarily closed due to the Suez Crisis. This event unfolded when Egyptian President Gamal Abdel Nasser nationalized the canal, leading to an international uproar. As a result, oil shipments from the Middle East to Europe were disrupted, causing a spike in oil prices. Nevertheless, the effects were relatively short-lived since the canal reopened within a few months.

In contrast, the longer closure initiated by the Six-Day War in 1967 and exacerbated by the Yom Kippur War in 1973 had profound, lasting effects on international trade, the global economy, and the geopolitical arena.

The Yom Kippur War led to an oil embargo imposed by the Organization of Arab Petroleum Exporting Countries (OAPEC), primarily targeting countries seen as supporting Israel, including the United States and the Netherlands. This embargo, combined with production cuts, caused a sharp increase in oil prices. Oil prices quadrupled, leading to what is often referred to as the “Oil Crisis of 1973.” This sudden and dramatic increase in energy costs had a ripple effect throughout the global economy.

Suez blockade – Public Domain

Shipping freight rates

I find it interesting getting an overview of what happened in the past and try imagining what could happen in a similar event today.

The closures of the Suez Canal in 1956 and 1967-1975 had significant impacts on freight rates in various shipping segments, including container shipping, tankers, and bulk carriers.

An interesting anecdote from the 1967-1975 closure is the story of Norwegian shipowner, Rilmar Reksten. Due to the closure, many ships couldn’t navigate the Suez Canal and had to take the longer route around the Cape of Good Hope. Reksten, owning a fleet of larger tankers capable of making this journey, saw a surge in demand for his services and amassed significant wealth during this period. This serves as a testament to how geopolitical events can reshape the dynamics of the shipping industry.

Below I made a brief overview of how freight rates were affected during these closures and what happened to rates after the re-openings:

| Period | Shipping Segment | Impact During Closure | Impact After Reopening |

|---|---|---|---|

| 1956 | Container | Limited impact due to early stages of containerization1. | Gradual expansion of containerization; rates stabilized with market fluctuations2. |

| Tankers | Increased rates due to longer routes (Cape of Good Hope)3. | Rates returned to normal; decline in oil prices with the shorter Suez route4. | |

| Bulk | Moderate increases in rates5. | Rates stabilized with the shorter Suez route reducing costs6. | |

| 1967-1975 | Container | Significant disruption; surged rates due to longer route around Africa7. | Rates stabilized; influence of market dynamics more than Suez Canal8. |

| Tankers | Sharp increase in rates due to disrupted oil shipments9. | Gradual decline in rates with shorter Suez route10. | |

| Bulk | Significant rate increases due to delays and costs11. | Stabilized rates with reduced transportation costs through the Suez12. |

In summary, the closures of the Suez Canal in 1956 and 1967-1975 had varying effects on freight rates across different shipping segments. These effects were obviously stronger during the longer closure, with significant rate increases in container shipping, tankers, and bulk carriers. After each reopening, rates gradually stabilized as the shorter Suez route reduced transportation costs, although market dynamics continued to influence fluctuations in freight rates in the years that followed. Nothing really surprising.

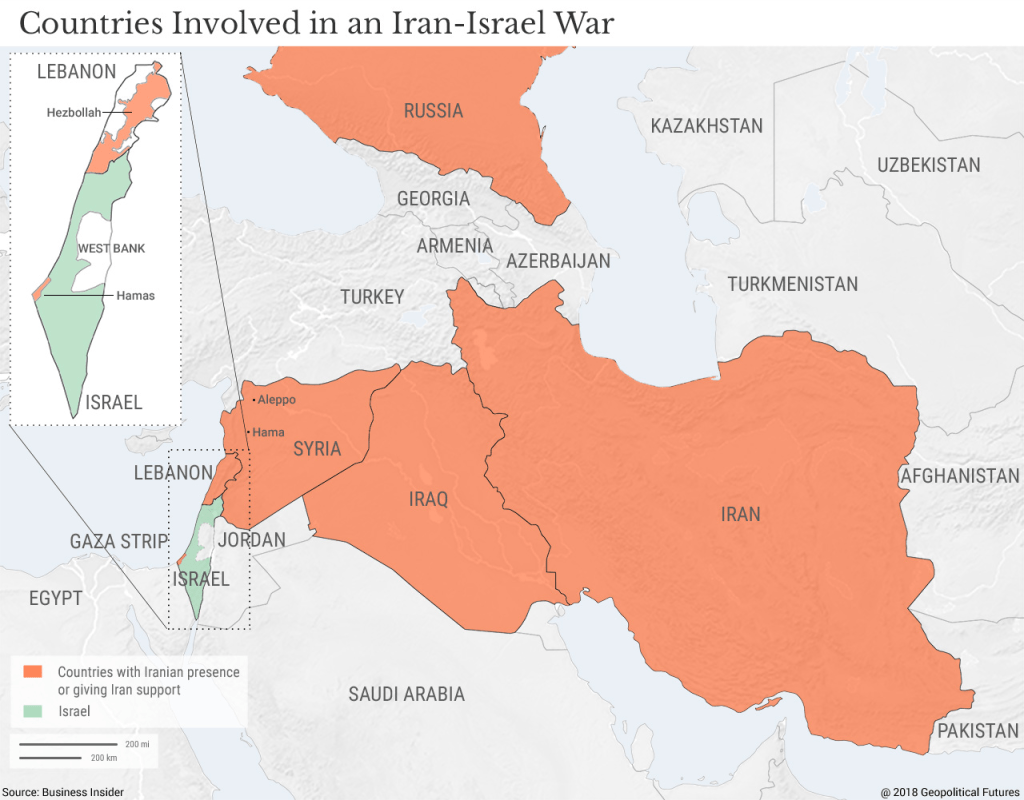

What if history repeats itself?

Image Source: Geopolitical Futures, 2018

In today’s world of intricate geopolitics and economic vulnerabilities, the potential for another regional war or a closure of the Suez Canal is a matter of significant concern. The current geopolitical climate, while distinct from bygone eras, still carries forward the echoes of past confrontations.

A looming concern in the backdrop of a wider conflict today is the possibility of an asymmetric war spearheaded by Iran and its proxies. Their objective might be to obstruct pivotal trade routes like the Hormuz Strait and perhaps the Suez Canal itself. Such a shift in the dynamics of conflict injects heightened uncertainty into an already complex situation.

If we were to experience disruptions akin to the brief Suez Canal closure of 1956, the world’s fragile economic state would be put to the test. Such interruptions would not only result in significant shipping delays but would also inflate shipping costs, leading to a domino effect on supply chains and worldwide trade.

Escalation of the current Middle Eastern tensions could exacerbate several existing global economic vulnerabilities13. Economic contraction could arise from hampered trade flows and escalated energy costs.

The recent conflict in Ukraine, which led to the restricted trade of vital commodities like crude oil, natural gas, and wheat, has already sent inflation rates soaring to unprecedented levels in many decades. Such heightened inflation has led to growing concerns about food security in different parts of the world and appears to be negatively influencing global economic growth. Current economic projections from the IMF indicate a potential decrease in global growth, dropping from 3.5% in 2022 to an estimated 3.0% in 2023, with a further decline to 2.9% expected by 202414.

As for shipping rates, should my hypothetical conflict materialize, the drivers for tankers and bulk carriers point towards elevated rates. This is primarily due to the vulnerable commodities market and concerns about lengthier supply routes, especially given the reportedly low order books for these segments in 2023.

The container market scenario is looking bleak after some golden years. Current freight rates for containers are notably low15 and there’s a record-breaking backlog of newbuilds deliveries16.

One of my professors often remarked on the paradoxical nature of the shipping industry: how natural and man made disasters, as unfortunate as they might be, are often good for shipping. The adage ‘One man’s misfortune is another man’s opportunity’ rings particularly true in this sector. Recall the story of Hilmar Reksten? Similarly, the COVID-19 pandemic presented both challenges and opportunities within the shipping industry. And while I anticipate that any significant conflict would indeed impact rates, I remain skeptical about them reaching the peaks seen in 2021 and 2022.

From my perspective, while there might be a brief resurgence I foresee a sharper downturn on the horizon, largely spurred by ongoing inflationary pressures.

The potential consequences of a broader regional war in the present day are deeply intertwined with the current geopolitical landscape and the fragile state of the global economy. It’s vital to remember that while I am reflecting on hypothetical scenarios, and these considerations highlight just how important global teamwork and resolving conflicts are for maintaining stable trade and a sound economy.

History often serves as a mirror to contemporary events. The Suez Canal closures remind us of the vulnerabilities in global trade networks. In today’s interconnected world, the importance of maintaining and safeguarding such vital trade routes can’t be overstated. As we navigate current geopolitical uncertainties, the lessons from the past can provide valuable insights into building a resilient future.

More than anything, my heartfelt wish is for the well-being of the people caught up in these situations, and for lasting peace and stability in the affected regions. After all, a stable and peaceful world benefits us all.

What are your thoughts on how the modern shipping industry can better prepare for such unforeseen disruptions? Share your insights in the comments below.

Bibliography

- Levinson, M. (2006). The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger. Princeton University Press. ↩︎

- Cullinane, K., & Khanna, M. (2000). Economies of scale in large containerships: optimal size and geographical implications. Journal of Transport Geography, 8(3), 181-195. ↩︎

- Stopford, M. (2009). Maritime economics. Routledge. ↩︎

- Yergin, D. (2008). The prize: The epic quest for oil, money & power. Free press. ↩︎

- Haralambides, H. E., & Londoño-Kent, M. P. (2004). Vessel size and the dry bulk freight market. Maritime Policy & Management, 31(4), 243-260. ↩︎

- Branch, A. E. (2007). Elements of Shipping. Routledge. ↩︎

- Cariou, P. (2011). Is the Suez Canal a substitute for or complementary to the Panama Canal?. Transport Policy, 18(4), 567-572. ↩︎

- Notteboom, T. (2006). The time factor in liner shipping services. Maritime Economics & Logistics, 8(1), 19-39. ↩︎

- Talley, W. K. (2013). Oil tanker operation and vessel sizes: A joint tanker project perspective. Transportation Research Part E: Logistics and Transportation Review, 54, 67-77. ↩︎

- McConville, J. (1999). Economics of maritime transport: Theory and practice. Informa. ↩︎

- Alderton, P. (2005). Port management and operations. Informa. ↩︎

- Goss, R. O. (1990). Economic policies and seaports: The economic functions of seaports. Maritime Policy & Management, 17(3), 207-219. ↩︎

- World Bank. (2020). Middle East and North Africa Economic Update: How Transparency Can Help the Middle East and North Africa. World Bank Group.https://openknowledge.worldbank.org/server/api/core/bitstreams/58ce62cb-f145-5d7c-a83b-22453f0beb1e/content ↩︎

- World Economic Outlook, Navigating Global Divergences. (October 2023). International Monetary Fund. Retrieved from: https://www.imf.org/en/Publications/WEO/Issues/2023/10/10/world-economic-outlook-october-2023. ↩ ↩︎

- Drewry. (2023). World Container Index Assessed by Drewry. Retrieved from https://www.drewry.co.uk/supply-chain-advisors/world-container-index-weekly-update/world-container-index-assessed-by-drewry ↩︎

- FreightWaves. (2022). Tidal wave of new container ships: 2023-24 deliveries to break record. https://www.freightwaves.com/news/tidal-wave-of-new-container-ships-2023-24-deliveries-to-break-record ↩︎

Leave a comment